Why I Won’t Buy a Million-Dollar HDB Flat (and Why You Might)

09 Jun 2023

by info Passion

The current state of the resale housing market has undoubtedly become much hotter compared to five years ago. Over the past couple of years, prices in the broader HDB resale market have been steadily increasing. One contributing factor to this trend is the delays in BTO construction caused by the pandemic. Additionally, the exceptionally low interest rates during the pandemic have led to a surge in demand for homes, not just in Singapore but globally, as it has become easier for people to obtain loans.

Another reason for the rising prices is the increasing number of flats reaching their Minimum Occupation Period (MOP). These newer flats tend to command higher prices compared to older flats in the same area. While it is worth noting that million-dollar HDB flats represent only a small fraction of the total HDB transactions, they have garnered significant attention.

Many of our readers have inquired about the viability of purchasing these million-dollar flats. In this article, I (Ruiming) will share my thoughts on why I am personally not inclined to buy one and why this perspective may also apply to you. However, it is important to clarify that we are not stating that buying a million-dollar HDB flat is inherently wrong. Some individuals may have valid reasons for considering such a purchase, which we will discuss later.

What makes a million-dollar flat?

A million-dollar resale HDB flat would typically have a few main qualities that allow it to command its hefty price tag.

The more of these qualities it has, the more likely it’ll reach the magical $1,000,000 price tag and beyond.

Size: The larger the flat, the more expensive it will be. This gives flats in less popular areas the ability to command higher prices. The recently sold jumbo flat in Yishun is one example.

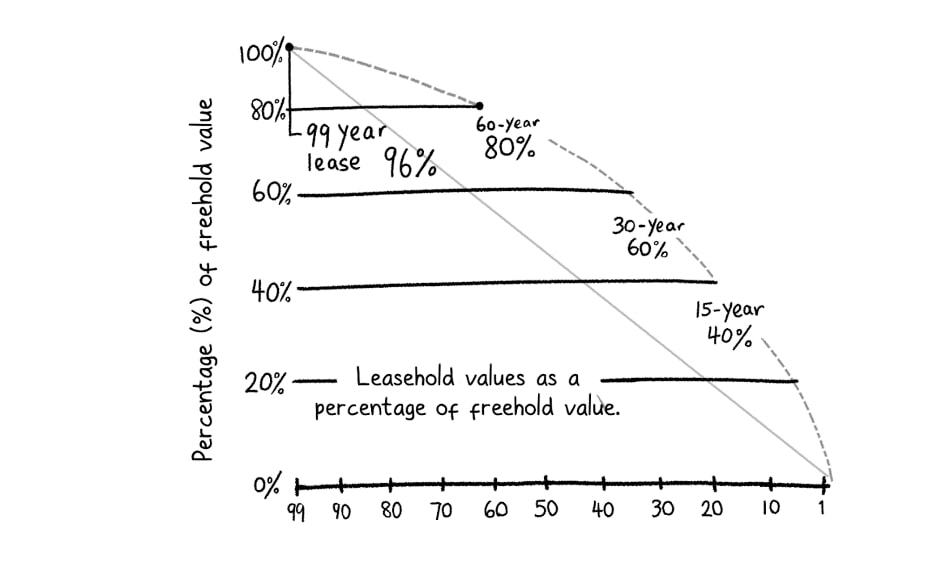

Lease: Generally, the newer the flat, the more expensive it will be, and vice versa. The Singapore Land Authority (SLA) has a rough guide known as ‘Bala’s Table’, which kinda shows how property prices are affected by their lease.

Older flats also have a limited pool of buyers, because if the lease of the HDB flat doesn’t last the youngest buyer till 95, there will be limitations on how someone’s CPF can be utilised.

Why is understanding Location, Size and Lease important?

Because these are effectively the trade-offs you have to make if you want to buy a home within your means.

Why you might not want a million-dollar flat

Why is it important to consider financial security when purchasing a home?

The reason is straightforward: allocating more money towards a home purchase means having less money available for other expenses. This aligns with the notion that every decision made in favor of something signifies a decision against something else. Therefore, it becomes crucial to keep financial security in mind while contemplating a home purchase.

Financial Security:

Buying an affordable home means financial security during turbulent times.

If we look at history, we can see that our adult lives, much like our parents', will have their ups and downs when it comes to the economy. This means there may be periods of unemployment and uncertainty.

To avoid added stress during tough times, it's a good idea to buy a flat that is comfortably within your financial means. This way, you'll have less to worry about when it comes to your mortgage.

Although millennials have mostly experienced low interest rates, it's important to remember that this hasn't always been the case. In the past, the Singapore Interbank Offered Rate (SIBOR) reached interest rates as high as 3.56% in 2006, and home loans exceeded 7% in the late 1990s.

For example, some readers who opted for floating mortgages during the pandemic are now starting to be concerned about potential interest rate increases. And rightfully so! Paying 3.85% interest instead of 1% on a significant loan can definitely add up.

Additionally, it's crucial to keep in mind that HDB flat prices don't constantly rise. From 2013 to 2019, both public and private property prices actually declined. The same can be seen in the late 1997 period, where the HDB resale index dropped by nearly 30% and only recovered in 2008.

If you're considering treating your flat as an investment, it's worth taking note of these factors.

Don’t pay *too much* for centrality and convenience

Time is valuable, and many argue that if you're financially savvy, it's wise to save time by living closer to the central business district (CBD) in a mature, convenient location. While this logic may seem sound, it's worth considering the following points:

Living in a more central and convenient area typically comes at a higher cost. This holds true in major cities like London, Tokyo, Paris, and Melbourne. If you have to work tirelessly to afford the price difference, it may not be worth it.

For instance, a couple earning a combined income of $20,000 might choose to buy a $900,000 flat in a central area to minimize their commute time. If they can comfortably handle the payments, it makes sense for them.

However, if you have to rely on borrowing from parents or find alternative ways to bypass loan limits, it's usually a sign that the convenience you desire is beyond your means.

It's important to note that not all workplaces are located in the CBD. There are several smaller commercial centers throughout the city, such as Jurong East, Paya Lebar, Changi, and One-North. Additionally, with flexible work arrangements, even if you do work in the CBD, you might find yourself going into the office less frequently.

If you're considering purchasing a car or motorcycle/scooter, the importance of being in a central location might not be as significant. When you choose to own private transportation, you're essentially paying for the convenience it provides.

In areas with limited public transport options, thinking outside the box can be beneficial. Based on personal experience, I've discovered that using a bicycle can often be a faster way to reach a destination within a 10 km radius. Alternatively, you can use a bike to cover the remaining distance to the MRT station.

By making this lifestyle change and receiving support from your workplace, you may not have to spend a significant amount of money on a unit in a central location.

Paying for space you don’t use

If I don't plan on having many children or staying child-free, having a large apartment would be unnecessary and would result in me spending more money. While having extra space is a luxury, especially in a city like Singapore where land is scarce, the real question is whether it is financially sensible. I do appreciate having enough personal space, but I don't want it to limit my freedom to pursue other things. Currently, my girlfriend and I are renting a 700 sq ft 3-room HDB flat, which is adequate, although I wouldn't mind being a bit happier with 900 sq ft.

Do you have enough for other life goals?

Having a place to call home is undoubtedly important. However, I believe it shouldn't be the sole focus of your aspirations in life.

Speaking from my own perspective, I have several personal goals that extend beyond just having a roof over my head:

1. I aspire to work overseas at some point, perhaps as a digital nomad, which would require a substantial amount of money, around $200,000, to cover living expenses.

2. Another goal of mine is to embark on an adventurous year-long cycling trip, which would require around $100,000 in funds.

3. Additionally, I desire the freedom to choose a job that I genuinely enjoy. To achieve this, I aim to have a passive income of at least $2,000 per month.

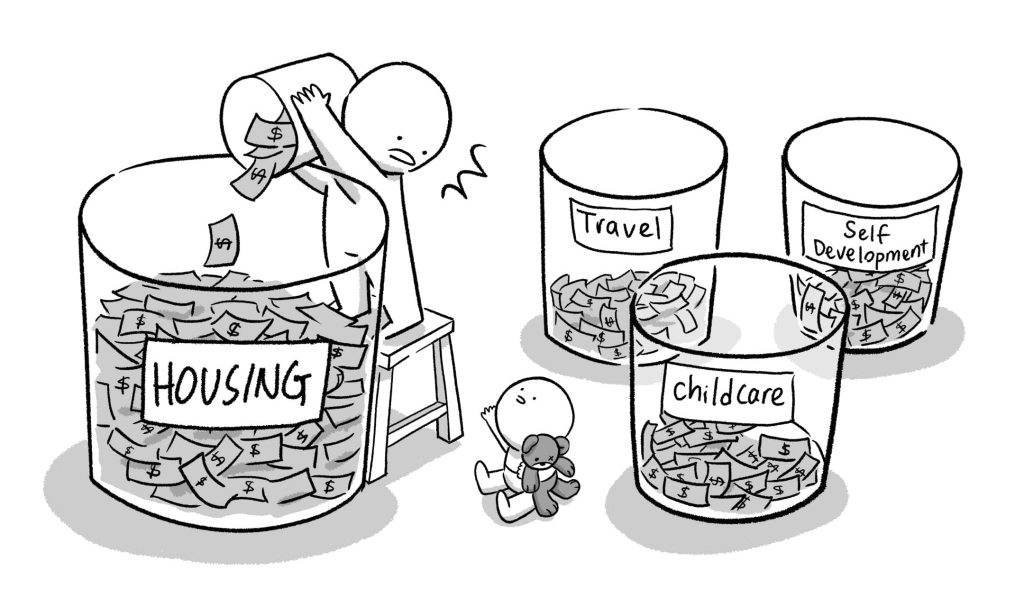

If I invest too much of my financial resources into buying a house, these goals will simply remain as distant dreams. Every extra dollar I spend on housing pushes me further away from realizing these aspirations.

Even if you're uncertain about your specific life goals, I believe it's wise to exercise caution when it comes to overspending on a home. The home you purchase can potentially limit the dreams you can pursue.

Therefore, if you find yourself contemplating the purchase of a million-dollar flat, it's essential to carefully consider the opportunity costs associated with such a significant investment in housing. Ask yourself if you are willing to accept the trade-offs that come with it.

So why do people buy million-dollar flats?

Having a roof over your head is undeniably important, but it shouldn't be the sole focus of your aspirations. Personally, I have a few goals in mind:

1. I aspire to work overseas at some point in my life, which would require a significant amount of money for living expenses, approximately $200,000. This ties into my desire to be a digital nomad.

2. Another goal of mine is to embark on an adventurous year-long cycling trip, which would require around $100,000.

3. I also want the freedom to choose a job that I genuinely enjoy, which means having a passive income of at least $2,000 per month.

If I spend excessively on a house, it will hinder the realization of these dreams. Every extra dollar allocated to housing moves me further away from achieving these goals.

Even if you're uncertain about your specific life goals, it's wise to be cautious about overspending on a home. The home you purchase can limit the possibilities and dreams you can pursue.

Therefore, if you're contemplating buying a million-dollar flat, carefully consider the opportunity costs associated with investing such a substantial sum in housing. Ask yourself if you're willing to accept the trade-off and if it aligns with your overall aspirations.

A final word about affordability

Yes, there is little question it’s a seller’s market right now. And will be for a while. Be prepared to pay more than pre-pandemic times.

However, what is also true is that there are many choices on the resale market.

The cheapest HDB flat on PropertyGuru is asking for $250,000 as of the writing of this article. The most expensive one? An eye-popping $1.65 million.

Our advice? Calculate what you can afford first above all else. Use your judgement to determine whether the seller’s asking prices are reasonable.

If you want to be extra safe, buy something below your means.

Otherwise, for peace of mind, buy something within your means.

And unless you want to spend the foreseeable future stressing about paying your mortgage, never spend beyond your means.

Stay woke, salaryman

A message from our sponsor, HDB

There are many factors that come into play when looking for a new home – the location, proximity to loved ones and amenities, size and more.

But amongst all of these, affordability is one of the key factors in making a housing decision. After all, housing would likely be one of your first biggest ticket purchases, so it’s important that your future home fits your budget and your needs.

If you’re looking for a new home, check out the guides, articles and resources available on MyNiceHome.

Also, check out past content pieces we’ve developed with HDB to navigate through your home-buying decision